Growth Factors Driving the Market: The Growth of the Cancer Diagnostics Market is driven mainly by increasing incidence of cancer and growth in the number of private diagnostic laboratories.

In an attempt to detect cancer in the early stages and bring down the mortality rate, governments in developed countries and primary care doctors are recommending cancer screening tests for patients. The US Preventive Services Task Force (USPSTF) recommends screening for colorectal cancer starting at 50 years of age to 75 years of age in the US as a means of preventing disease incidence and ensuring early-stage treatment. Canada has also implemented guidelines for biennial colorectal cancer screening for people aged 50 to 74 years.

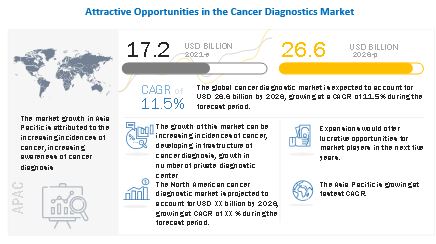

MarketsandMarkets™ View on Revenue: The global cancer diagnostics market size was valued at USD 17.2 billion in 2021 and is expected to grow at a CAGR of 11.5%

Industry Segmentation in Detailed:

The consumables segment is expected to grow at the highest CAGR during the forecast period.

Based on the product, the cancer diagnostics market is segmented into consumables and instruments. The consumables segment is projected to witness the highest growth during the forecast period. The repeated purchase and high consumption, and the high prevalence of diseases the major factors supporting the growth of this segment.

The technology segment accounted for the largest share of the cancer diagnostics market.

By technology, the cancer diagnostics market is segmented IVD testing, imaging based and biopsy technique. The IVD testing segment accounted for the largest market share in 2020. The large share of this segment can be attributed to increasing incidence of cancer.

Hospitals for the largest share of the cancer diagnostics market.

Based on end-users, the cancer diagnostics market is segmented into hospitals and diagnostic laboratories. The hospitals segment accounted for the largest share of the cancer diagnostics market in 2020. The increasing number of patients visiting hospitals, rising number of in-house diagnostic procedures performed in hospitals, and growing awareness regarding early diagnosis is are the major driving factor for this market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=186559121

Leading Key Players Analysis:

Some of the major players operating in this market are GE Healthcare (US), Roche Diagnostics (Switzerland), and Becton, Dickinson and Company (US). In 2020, GE Healthcare held the leading position in the market. The company has a strong geographic presence across the US, Asia, Europe, Middle East and Africa, & the Americas. Moreover, the company’s strong brand recognition and comprehensive product portfolio in the cancer diagnostics market is its key strength. BD held the second position in the cancer diagnostics market in 2020.

Geographical Trends in Detailed:

The cancer diagnostics market is segmented into four major regional segments, namely, North America, Europe, Asia Pacific, and the Rest of the World. In 2020, North America accounted for the largest share of the cancer diagnostics market. The large share of North America can be attributed to factors such as the increasing incidences of cancer, growing awareness early diagnosis and technological advancement.

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=186559121