The Regenerative Medicine Market growth is driven by rising investments in regenerative medicine research, and the growing pipeline of regenerative medicine products, and the increase in prevalence of chronic diseases, genetic disorders, and cancer.

Growing prevalence of chronic diseases, genetic disorders, and cancer;

Over the last few decades, the incidence and prevalence of chronic diseases such as CVD, cancer, diabetes, ulcers, and genetic disorders such as cystic fibrosis have increased significantly across the globe. Diabetes and obesity can result in the increased incidence and complexity of wounds such as infections, ulcerations (leg or foot ulcers), and surgical wounds, which require treatments and incur exorbitant medical expenses.

Opportunity: Implementation of the 21st Century Cures Act;

The 21st Century Cures Act was signed into law in the US in December 2016. Among other objectives, this new law has been enacted to advance regenerative medicine research and medical innovation and covers various provisions that may impact the development and approval of several products in the coming years.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=65442579

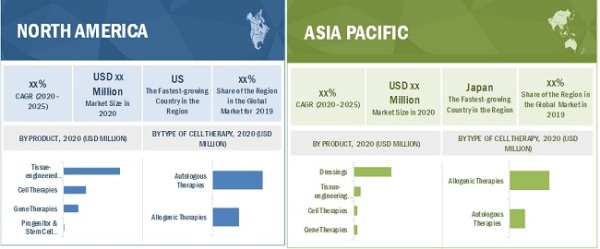

The tissue-engineered products segment accounted for the largest share of the Regenerative Medicine Market.

Based on products, segmented into tissue-engineered products, cell therapies, gene therapies, and progenitor and stem cell therapies. The tissue-engineered products segment accounted for the largest share in the market in 2019. The increasing adoption of tissue-engineered products for the treatment of chronic wounds and musculoskeletal disorders and the rising funding for the R&D of regenerative medicine products and therapies are the major factors driving the growth of this segment.

Oncology segment to register the highest growth rate during the forecast period

Based on applications, the Regenerative Medicine Market is segmented into musculoskeletal disorders, wound care, oncology, ocular disorders, dental, and other applications. In 2019, the oncology segment accounted for the highest growth rate. This can be attributed to the rising prevalence of orthopedic diseases, growing geriatric population, increasing number of stem cell research projects, growing number of clinical researches/trials, and the rich pipeline of stem cell products for the treatment of musculoskeletal disorders.

Request Research Sample Pages:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=65442579

Recent Developments:

– In February 2020, Integra Lifesciences (US) launched AmnioExcel Plus Placental allograft membrane.

– In November 2019, Stryker Corporation (US) acquired Wright Medical (US) to strengthen its product portfolio.

– In March 2019, Smith & Nephew (UK) acquired Osiris Therapeutics (US) to strengthen its product portfolio.

North America is the largest regional market for Regenerative Medicine Market

The market is segmented into four major regions, namely, North America, Europe, Asia Pacific, and the Rest of the World (RoW). In 2019, North America accounted for the largest share in the market. The growth in the North American market can be attributed to rising stem cell banking, tissue engineering, and drug discovery in the region; expansion of the healthcare sector; and the high adoption of stem cell therapy and cell immunotherapies for the treatment of cancer and chronic diseases.

The major players operating in this Regenerative Medicine Market are 3M (US), Allergan plc (Ireland), Amgen, Inc. (US), Aspect Biosystems (Canada), bluebird bio (US), Kite Pharma (US), Integra LifeSciences Holdings Corporation (US), MEDIPOST Co., Ltd. (South Korea), Medtronic plc (Ireland), Anterogen Co., Ltd. (South Korea), MiMedx Group (US), Misonix (US), Novartis AG (Switzerland), Organogenesis Inc. (US), Orthocell Limited (Australia), Corestem, Inc. (South Korea), Spark Therapeutics (US), APAC Biotech (India), Shenzhen Sibiono GeneTech Co., Ltd. (China), Smith & Nephew plc (UK), Stryker Corporation (US), Takeda Pharmaceutical Company Limited (Japan), Tego Science (South Korea), Vericel Corporation (US), and Zimmer Biomet (US).

Speak to Analyst:

https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=65442579